![]()

Friday’s release of the May employment report will offer important insights into the economy’s health.

Conference Board Consumer Confidence Index:

May (Tuesday)

Consumer confidence fell last month as views on current economic conditions worsened. Surveyed consumers indicated that a weakening job market was a contributing factor.

- Expected/prior consumer confidence: 92.0/93.8

- Actual consumer confidence: 93.1

Personal Income and Personal Spending:

April (Thursday)

Personal income was unchanged in April, below expectations, while spending rose a solid 0.5 percent.

- Expected/prior personal income monthly change: +0.4%/+0.5%

- Actual personal income change: +0.0%

- Expected/prior personal spending monthly change: +0.5%/+1.0%

- Actual personal spending change: +0.5%

Equity

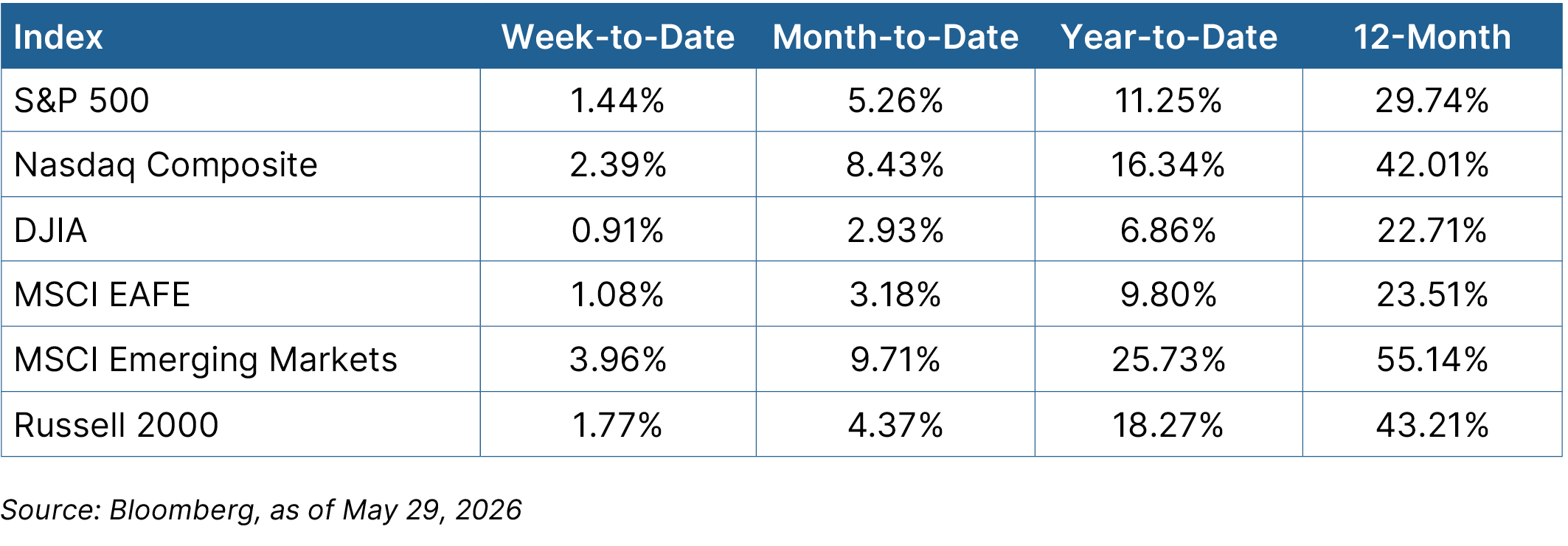

U.S. markets rallied across the board again. Continued hopes for a negotiated end to the war in the Middle East led to a 9.6 percent drop in oil prices. The Nasdaq and S&P 500 closed at record highs, and the Russell 2000 rallied 1.77 percent. The technology sector led markets higher, rising 4.56 percent. Unsurprisingly, the energy sector declined 5.43 percent. International markets rose.

Fixed Income

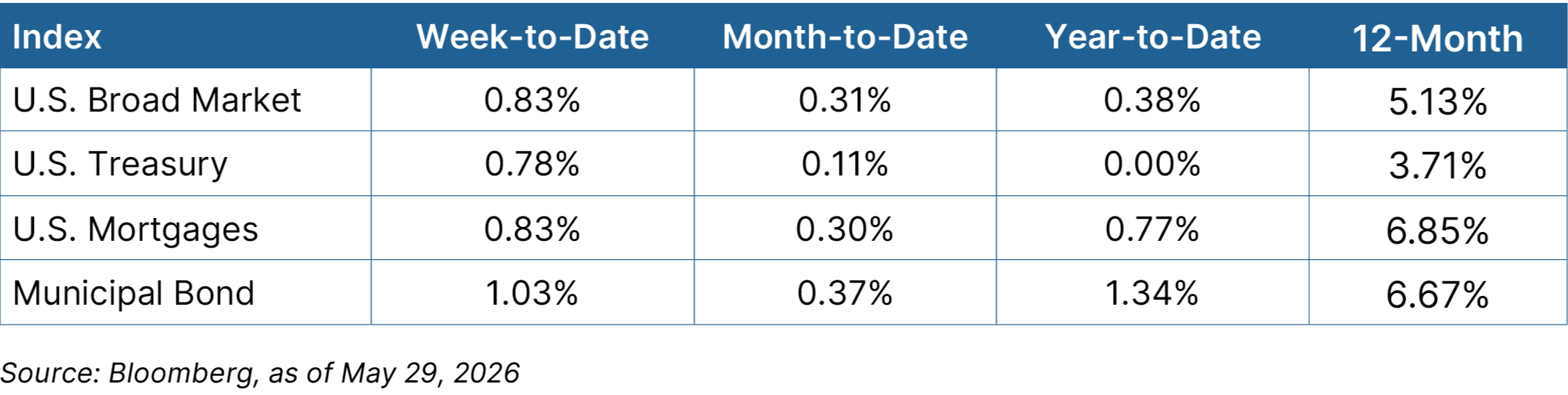

Fixed income markets rallied on developments in the Middle East. Lower oil prices alleviated some concerns about accelerating inflation. Treasury yields declined across the board, with the 10-year closing at 4.43 percent. High-yield bonds and municipal bonds moved higher.

Looking Ahead

The health of the labor market will be in focus this week.

- The week kicks off on Monday with the Institute for Supply Management (ISM) Manufacturing index for May. It’s expected to improve modestly.

- On Wednesday, we’ll see the ISM Services index for May. Economists expect a modest improvement.

- The week wraps up on Friday with the employment report for May. Hiring is expected to slow, with 93,000 new jobs anticipated.

- Earnings reports continue this week, highlighted by Broadcom’s report on Wednesday.